Imagine the following hypothetical scenario: you are resident in Luxembourg, happily married, and have owned a beautiful apartment on the Belgian Coast (Knokke-le-Zoute, if we're being specific) since 1985.

Following this hypothetical situation, let's say the property is worth €1,100,000 and bequeathed to the surviving spouse, then to your son who lives in France. With this situation, the entire property appears to be a pleasant gift for your heir, whose future should be guaranteed.

However, inheritance rights in Luxembourg can quickly transform such a dream scenario into a nightmare, especially if your estate or heirs have travelled. Continuing the above scenario, here is an example of how inheritance could quickly turn ugly:

In total, the heir could be looking at more than €600,000 in death duties, corresponding to a staggering 60% of the apartment's value. As lawyer François Derème explains, the son in this situation would really have to love Knokke-le-Zoute to agree to pay the death duties out of his own pocket and keep his parents' apartment.

Granted, this hypothetical scenario of the Knokke-le-Zoute apartment is certainly a rather disastrous example of inheritance turning into a fiasco, but according to Derème, it is certainly plausible. The lawyer is a specialist in inheritance and hosted a conference at the Cercle Cité last week.

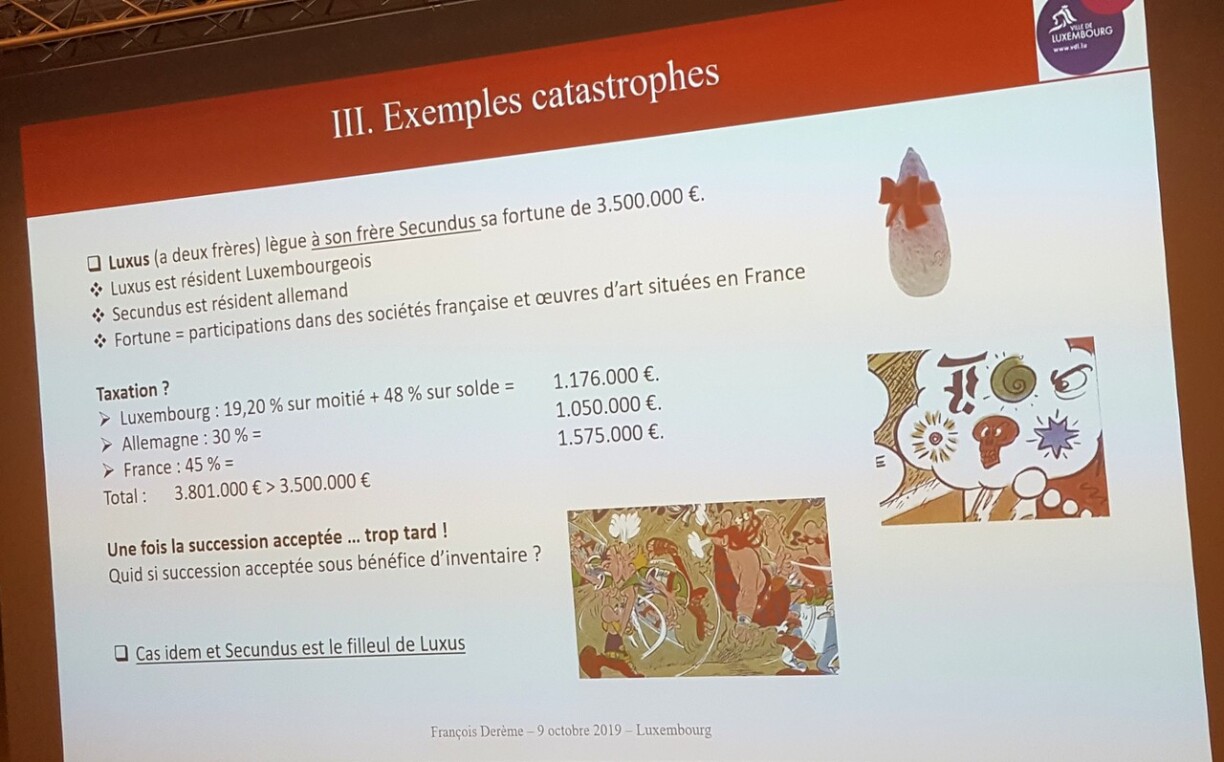

Derème cited a far more catastrophic example, as seen in the slide below. Luxus is a Luxembourgish resident and designates brother Secondus , who resides in Germany, as his heir to his €3,500,000 fortune. The fortune in question comprises shares in French businesses and artwork in France and is quickly subject to a staggering amount of tax in Luxembourg, Germany, and France. Ultimately in this scenario, the €3,500,000 inheritance becomes a debt of €3,801,000.

Whilst inheritance might be straightforward if all those concerned and the estate in question is based in Luxembourg, it becomes both more complicated and costly once other countries are involved. And which country gives pensioners cold sweats? France takes that crown in the Greater Region, Derème announced, while pointing out the different risks of double or even triple taxation in the event of a succession. The lawyer broke down the different points as following:

The question following all this information is whether safeguards exist to prevent taxes from overlaying each other. As the inheritance lawyer explained, simply put, there are no safeguards at an international level. Derème said it is puzzling that Luxembourg, an economic and financial hub known to have one of the highest amounts of collective agreements, has no such agreements in terms of donations and inheritance.

However, national law does outline measures preventing double taxation, albeit distinguishing between movable and real estate assets based abroad.

For real estate assets, if a Luxembourgish resident dies with real estate abroad, the heir in question is exonerated from paying rights in Luxembourg. As for movable assets, heirs are exonerated if they fulfil three cumulative criteria, namely that the inheritance tax was levied in the country where the movable assets are found, inheritance tax was taken abroad based on the deceased's citizenship, and if the heir supplies a receipt and certificate from the foreign tax authority.

All in all, inheritance is a rather complicated issue, especially when it comes to a population so prone to moving around as the population of Luxembourg. In the spirit of saving money and not being caught out once it is too late, it is certainly worth consulting a specialist.