RTL Today recently launched a survey in connection with home-based working to see how keen people are to return to the office post-pandemic. The headline of the article was that only 8% of respondents want to return full time – so not a lot of people seem to be excited at the prospect of returning to the pre-pandemic status quo!

First of all, we want to make it clear that we are not writing this article to say what the best policy is for employers to adopt for home-based working. We merely want to explain the rules.

First up is the tax side – no doubt a lot of people’s favourite topic! When we look at an individual’s tax situation, the first and most important fact to establish is where that person is considered to be resident for tax purposes. To keep things simple, let’s assume that an individual is a tax resident where they live with their family. This is an important point, as the country where someone is a tax resident is the country that has the right to tax the person on their worldwide income – irrespective of where the income is sourced from.

For a Luxembourg tax resident with a Luxembourg employer, things are pretty straightforward from a tax perspective, they will be fully taxable in Luxembourg in connection with their employment income, even if they have business trips outside of Luxembourg.[1]

Where the tax side of things becomes more complex is within the context of cross-border workers. We have over 200,000 cross border employees in Luxembourg, the majority of whom are resident in France, Belgium and Germany. For non-Luxembourg tax residents, their exposure to taxes in Luxembourg is limited to what is considered as Luxembourg source income. For employment income what this means is that they are taxable in Luxembourg in connection with the income related to the days physically exercised in Luxembourg.

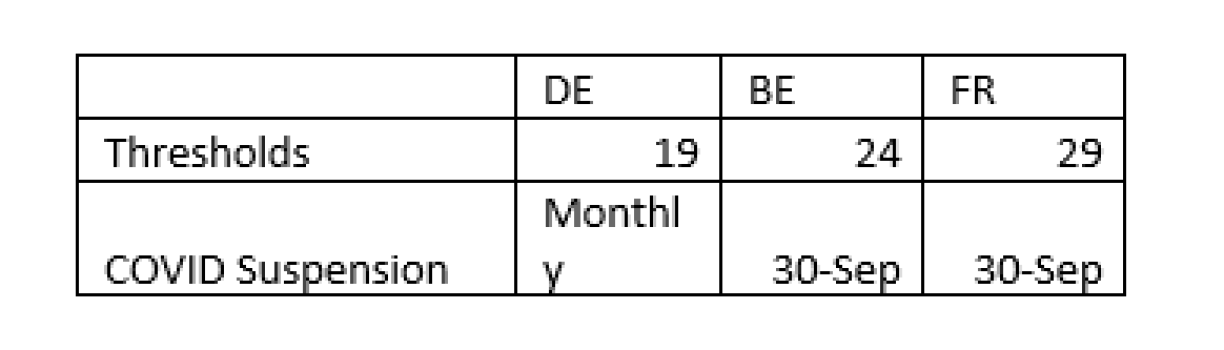

Over the past number of years, mutual agreements have been agreed between Luxembourg and the neighbouring countries. As an exception to the principle that the salary related to any workday spent out of Luxembourg is taxable in the country of residence, the mutual agreements introduced tolerance thresholds. 19 days for German residents, 24 for Belgian residents and 29 for French residents.

It is important to be clear that the tax thresholds refer to non-Luxembourg workdays, NOT just work days spent in the country of residence. As such, the thresholds include days spent going on business trips outside of Luxembourg as well as days spent working from home in the employee’s country of residence.

If a non-resident employee of a Luxembourg company does not exceed these thresholds they remain fully taxable in Luxembourg.

However, if a non-resident employee exceeds the threshold applicable to their country of residence, they are taxable in their country of residence as from the first day in connection with the employment income related to the non Luxembourg workdays.

Due to the pandemic, the rules related to the application of the tax thresholds were suspended to encourage those who could to work from home.

_______________________________

[1] Nonetheless, even for Luxembourg resident employees, an employer should ensure to be compliant from a Regulatory and Employment Law perspective within the context of home-based working.

Belgium and France have confirmed that the thresholds are currently suspended to 30 September 2021. For Germany the suspension is extended on an implied monthly basis until either country indicates otherwise.

In any event, we will soon arrive at the situation whereby these thresholds will once more be applicable, either in October or later in the year / next year.

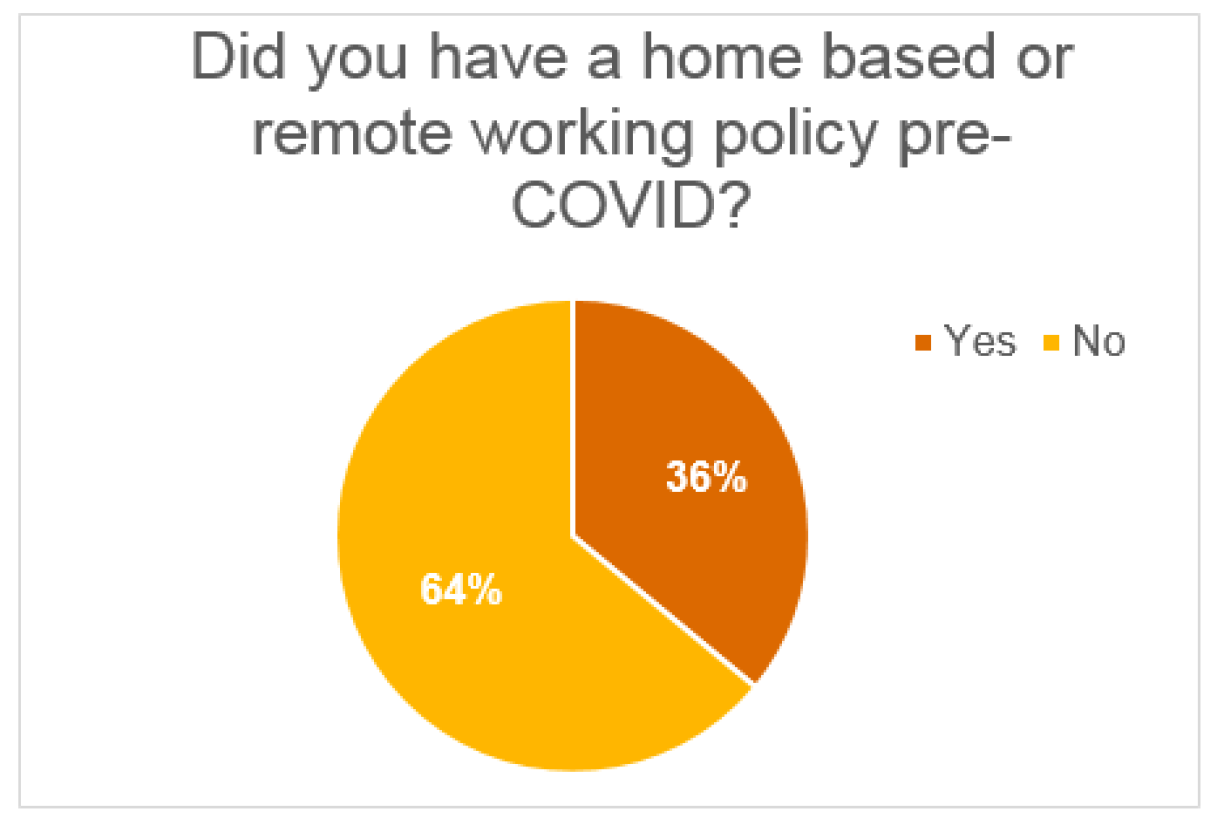

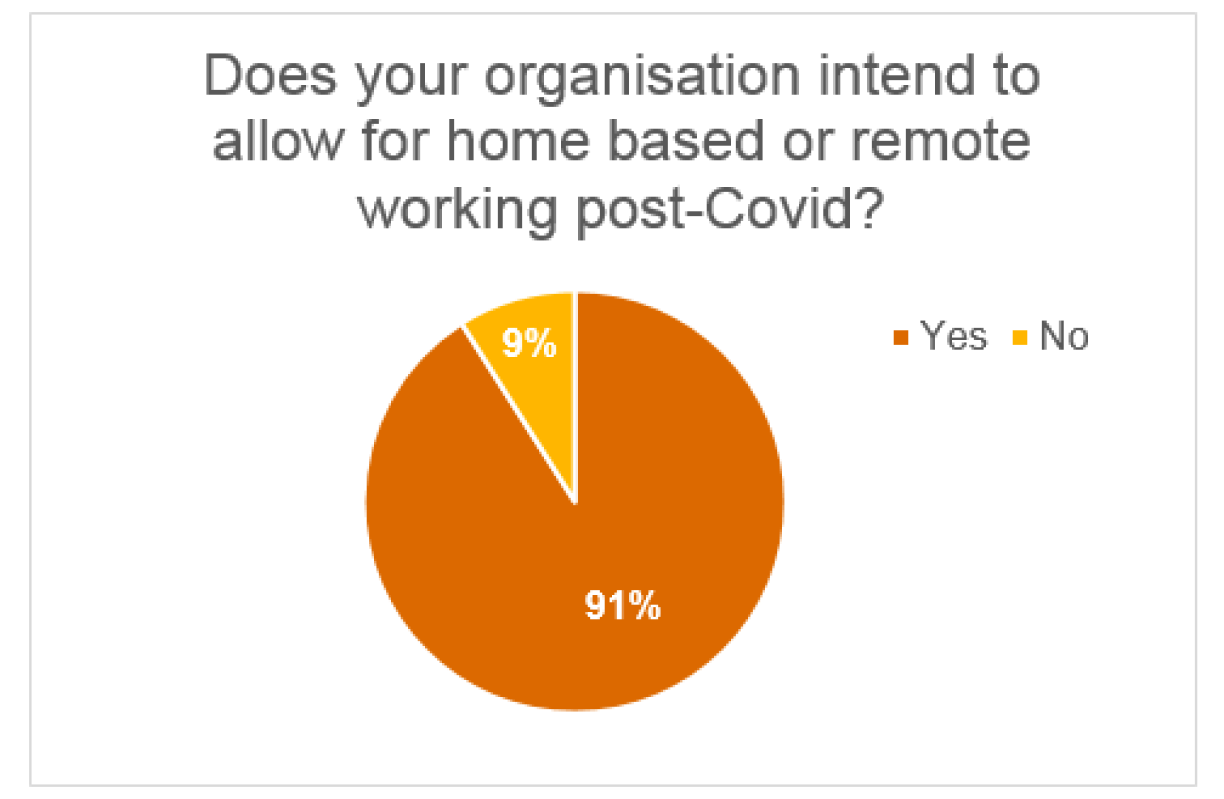

Pre-pandemic, we already saw that flexible working or home-based working was becoming an important topic for many organisations located in Luxembourg. What we now see is that since March last year, this trend has been accelerated– many organisations have come to realise that it is possible to be flexible around how an employee’s work is organised without a negative impact on productivity.

Employees themselves have seen the benefits of being able to work from home for at least part of the time. The result is that home-based working has now been pushed to the top of the agenda for a large number of Luxembourg employers.

PwC undertook a survey of Luxembourg employers in May of this year, and the responses received are quite telling.

We can see that there has been a fundamental and dramatic shift in employers’ priorities around home-based working pre- and post- COVID-19. It is clear that for an employer the implementation of a home-based working policy will be a differentiator in attracting and retaining talent.

So what does home-based working translate to in practice for a cross-border employee and their Luxembourg employer?

Working just one day a week outside of Luxembourg will have employment tax and personal tax consequences for the non-resident employee as well as for the Luxembourg employer. One day a week works out to around 50 days a year, so quite clearly for all cross-border workers this would exceed the respective tax thresholds.

Luxembourg employers need to be able to track employees’ work locations to identify when an employee is working from home, or on a business trip outside of Luxembourg. They will need to ensure that the income related to the non-Luxembourg workdays is exempted in the Luxembourg payroll. The Luxembourg employer may even have registration obligations in the other country to withhold taxes in that country.

Having to register as an employer in another country is no small undertaking – it will come with a real administrative and financial cost. This obligation for the Luxembourg employer is particularly relevant for organisations who have French tax resident employees. Since 2020 there are two types of withholding tax obligations in France – the first in connection with the French work days whereby the Luxembourg employer will need to register in France and withhold taxes and the second in connection with 3rd country workdays (workdays outside of Luxembourg and France) where the individual will need to arrange for the taxes to be withheld on the income related to those workdays via their income tax return.

It is also possible, depending on the situation, that similar withholding obligations may arise in Belgium and Germany for a Luxembourg employer.

The implications of split taxation for an employee will differ depending on where they are tax resident. For example, for a Belgian, German and a French resident employee who earn the same income, and who exceed the threshold in their country of residence, the impact on their net take home pay will be different. They may take home less than if they remained fully taxable in Luxembourg. Conversely, in some situations they may come out with a net increase. What the impact will be depends on the country of residence, extent of split taxation, family situation and many other factors.

Finally, having exempt income in Luxembourg may also impact a non-resident employee’s tax class for Luxembourg withholding tax purposes, whereby they may no longer qualify for tax class 2.

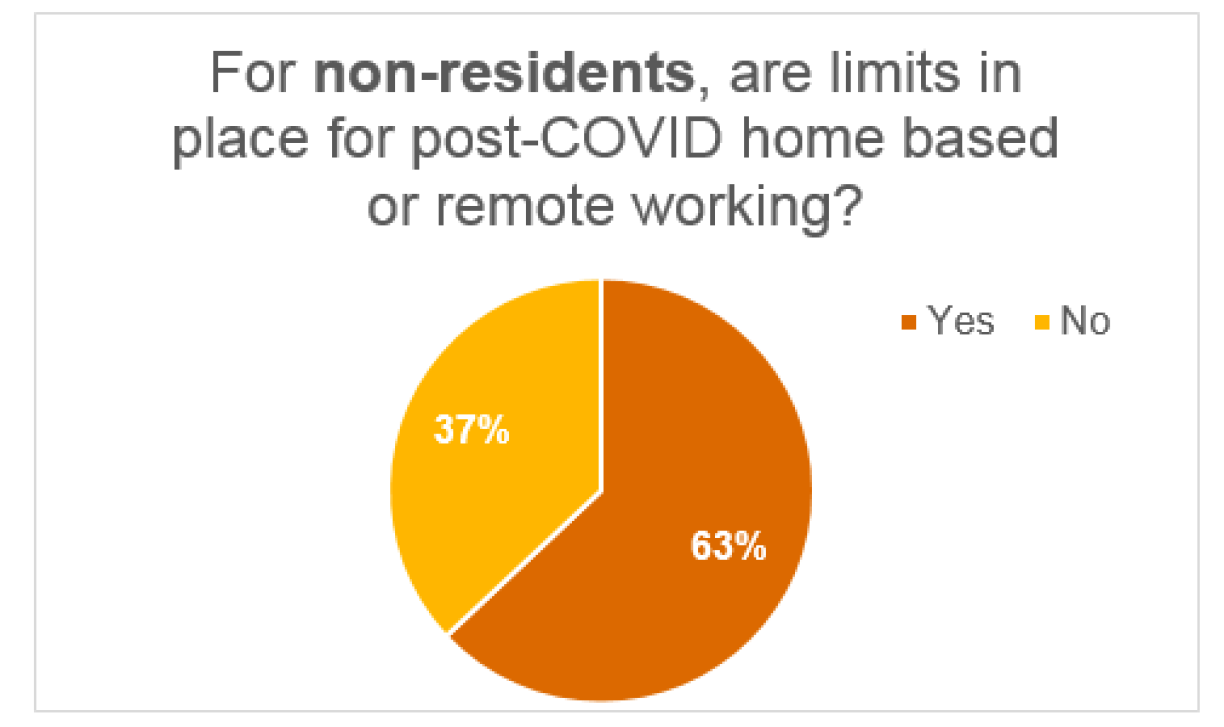

So, we can see that the consequences of working just one day week outside of Luxembourg can be rather complex to manage for an organisation with non-resident employees.

This may be the reason why over 20% of the respondents to the PwC survey indicated that they will use the tax thresholds as the limit to which they can allow home-based working for non-resident employees. We also see that different limits may apply to Luxembourg resident employees, as for this employee population the tax implications are less complex.

However, A number of organisations indicated they were willing to go beyond the tax thresholds. For these organisations we can see that the limit or red line for them is the threshold which applies in connection with social security. Social security rules are regulated at European level[2] and are completely separate to the tax rules we have been looking at up until now.

As a default, a non-resident employee of a Luxembourg employer is affiliated to the Luxembourg social security system. The Luxembourg social security system is a very generous system with regards to family allowances, health and pension benefits.

But, if a non-resident employee spends more than 25% of their time working from their country of residence, this will mean that they should not be affiliated to the Luxembourg social security system anymore, but should in fact be affiliated to the social security system in the country of residence.

Similar to the tax thresholds, the application of the 25% threshold has been suspended due to the pandemic. Belgium and Germany have confirmed they have suspended the application of the threshold until 31 December 2021. France has up until now confirmed the suspension of the 25% threshold to 30 September 2021 (but we anticipate this will be pushed to 31 December 2021).

25% of working time works out at just over one day a week working from home. Changing the social security system of affiliation can have a major impact on the employer costs. It would also have a material impact on the cost for the employee, not only in terms of the levels of contributions but also in connection with the loss of related benefits. There would also be administrative and compliance obligations on the Luxembourg employer to register in the other jurisdictions and operate multiple payrolls so as to calculate and pay over social security to the authorities abroad.

We see in the market that the majority of employers are reflecting on how they can provide flexibility to their employees. However, the different limits which exist in connection with personal taxes and social security mean that it is a complex subject. In addition to these important points an employer must also ensure to assess a myriad of other points within the context of implementing a home based working policy – employment law, regulatory obligations, corporate tax implications. Not to review all these aspects within the context of the implementation of a home-based working policy may lead to an employer not being compliant in Luxembourg or even abroad.”

[1] Nonetheless, even for Luxembourg resident employees, an employer should ensure to be compliant from a Regulatory and Employment Law perspective within the context of home-based working.

[2] Regulation EC n°883/2004 on the coordination of social security systems