The summer months confirmed the slowdown in US economic growth, as mounting evidence of a stalling labour market strengthened the case for a first interest rate cut in 2025.

The European Union and the United States secured a trade agreement that closely resembles the accord struck between the US and Japan. The deal will lock in tariffs at 15% on most EU goods imported to the US – including cars and pharmaceutical products. While the agreement does provide more stability and draws a line under uncertainty, the hike in customs duties to 15% is still significant enough to act as a drag on business. The deal also includes commitments to invest in the United States, demanded by the Trump administration. For example, under the agreement, Europe was required to commit to $250 billion in annual energy purchases (oil, gas, and nuclear technology) over the next three years. But this target seems unworkable. To hit it, the European Union would have to triple its energy imports from the US from $75 billion in 2024 (out of $400 billion in total energy purchases). A target that seems unrealistic, especially as energy is imported by private companies whose decisions are dictated by the market (price fluctuations, etc.) rather than political considerations.

US economic growth softened during the first half of the year as annual GDP growth slowed to 1.4%. The slowdown is pronounced and broad-based across all components of domestic demand. Consumer spending, the engine of the US economy, slowed to an annual rate of 1% over the first half of 2025. As a result, it stands to reason that investors are scrutinising developments in the labour market even more closely. And the deterioration is stark.

The steep downward revision in new jobs figures for May and June announced by the Bureau of Labor Statistics (BLS) riled President Trump. He fired the head of the independent agency responsible for employment and inflation statistics on the first of August. Claiming that the figures were manipulated for political reasons, the US President’s decision will ultimately be counterproductive, as it will likely undermine investor confidence in BLS reports. The August jobs data did little to reassure. The US economy added only 22,000 jobs, confirming the labour market’s anaemic performance since May. And the unemployment rate worsened, rising to 4.3%, its highest since 2021, despite lower migration flows and no significant increase in the pace of layoffs.

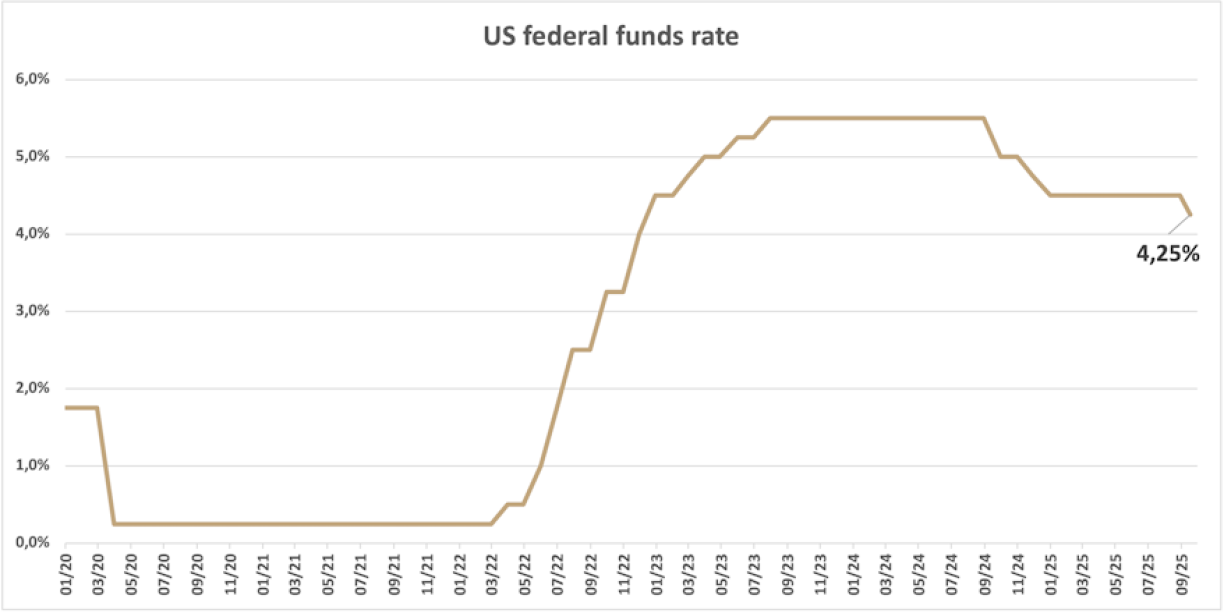

Downside risks to the jobs market over the past few months prompted the US monetary policy authority to shift its position, even though inflation still hovered around 3%. The recent quarter-point cut came as no surprise to the markets, which have priced in almost two further rate cuts by the end of 2025.

Source: Federal Reserve, Banque de Luxembourg

The move to lower rates comes amid intense political pressure on the Fed, especially on Chairman Jerome Powell, whose term ends in May 2026. Powell has come under fire for failing to accede to President Trump’s demands for steep rate cuts.

Donald Trump appointed his economic adviser Stephen Miran, an acerbic critic of the Fed’s current policies, to the Federal Reserve’s board of governors. He will temporarily replace Adriana Kugler, who is resigning. Miran’s appointment to the board was confirmed in record time by the Senate. He will now add his voice to those of the two other Trump picks, Christopher Waller and Michelle Bowman, in support of lower interest rates. Even more worrying, and with no legal basis whatsoever, the US President said he was firing Fed Governor Lisa Cook, accusing her of making false statements on a mortgage application. Cook, who was appointed by Joe Biden in 2022, has refused to step down. In all probability, the Supreme Court will have to weigh in and decide whether Mr Trump has cause to fire Lisa Cook.

The Trump administration’s aim is crystal clear: to subordinate monetary policy to its very expansionist fiscal policy. In sum, the independence of the Federal Reserve is under attack to keep rates low and cut borrowing costs. This “fiscal dominance” is cause for concern, since it threatens the very credibility of the institution whose remit is essential for the economy and financial markets to function smoothly. The administration risks generating upward pressure on inflation and pushing long rates higher. This is ironic, to say the least, since Donald Trump's promise to tame inflation was probably what won him the election.

The greenback is set to slide further as the Trump White House continues its assault on the US central bank. Although appetite for US assets remains strong, many investors, especially in Asia, are increasingly hedging their exposure to the dollar.

We think a firm bet on the outlook for the dollar is risky at this stage. Currencies move relative to other currencies. Fluctuations are influenced by many factors, not just differences in interest rates or growth rates.

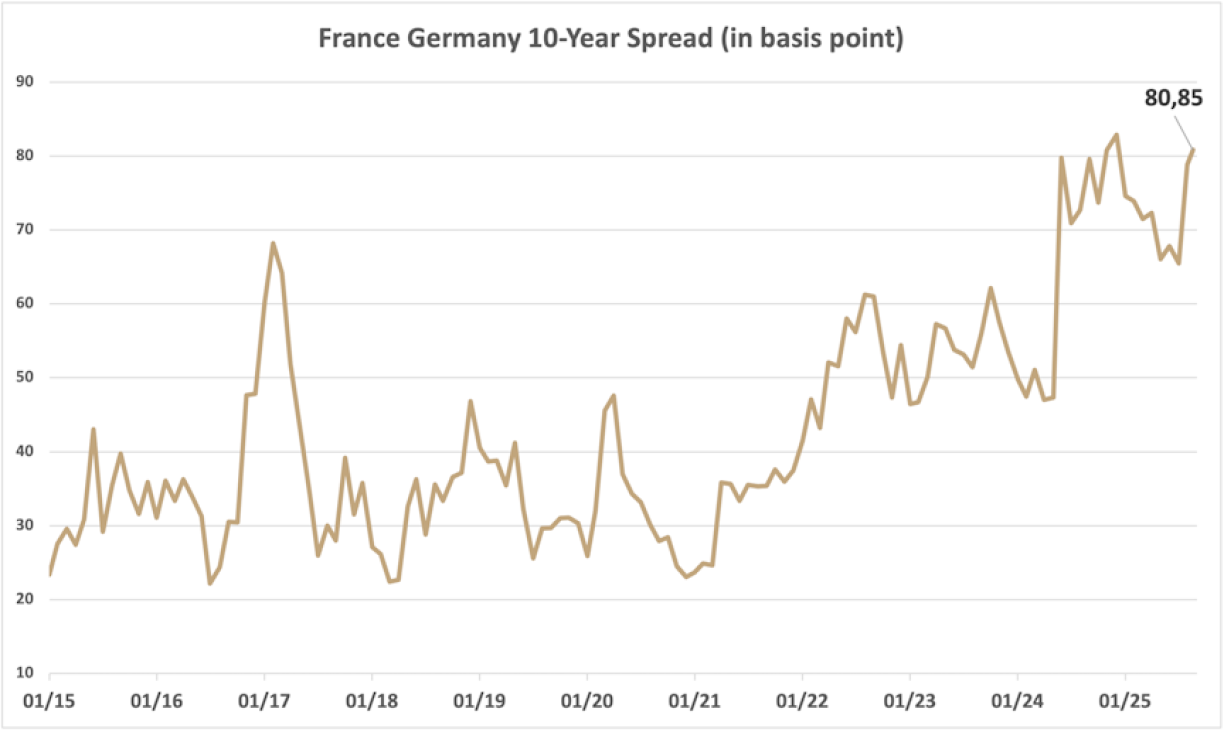

The euro has shrugged off escalating political risk in France. The markets had priced in Fitch Ratings’ downgrade of France from AA- to A+. But the country’s public finances are troubling. France’s deficit will exceed 5% of GDP in 2025 and is set to remain above this threshold in 2026 and 2027. In an extremely polarised country, the new French Prime Minister, Mr Sébastien Lecornu, must quickly find a compromise on the budget that will not damage growth. Parliament urgently needs to pass credible measures to reduce the deficit and shrink the public debt. According to the latest estimates by the International Monetary Fund, the French debt pile was 113% of GDP at the end of 2024. It expects that ratio to soar to 130% by 2030. Although the French-German 10-year yield spread hasn't widened, it is testing the highs recorded over the past 10 years at close to 80 basis points.

Source: Bloomberg, Banque de Luxembourg

The complex political environment in France doesn’t seem to be worrying the European Central Bank. It reminded markets that it has the tools (the transmission protection instrument) to intervene in the secondary market in the event of an "unwarranted and disorderly" rise in borrowing costs, which isn’t called for by the current situation.

The ECB has held deposit rates unchanged at 2%. Inflation is back on target at an annual rate of 2% in August, and PMI leading indicators are on the right path. The composite index ticked higher to 51.1 (vs 50.6 expected and 50.9 in July) on an expanding manufacturing sector (50.5 points vs 49.8 the previous month) as order books filled up for the first time in over a year. Despite tariff shocks and the steep rise in the value of the euro, the eurozone economy has held up well. The ECB raised its growth outlook to 1.2% for 2025 (from 0.9% previously), followed by 1% in 2026 and 1.3% in 2027. It expects inflation to hold steady at under 2% for the next two years. Southern European economies have built up strong momentum. Take Portugal: Fitch Ratings has just upped its rating to A from A- on the strength of healthier public finances and solid growth, expected to be just under 2% in 2025 thanks to a buoyant labour market.

Artificial Intelligence powered global equity markets higher over the summer months. Market concentration intensified in the US. The top 10 S&P 500 companies by market capitalisation made up around 40% of the index. US valuations still seem stretched but are supported by solid earnings growth and high profitability. The fall in the dollar is not good news for euro-denominated investors and has wiped out much of the gains made at the start of the year.

Damien Petit, Head of Private Banking Investments,

Banque de Luxembourg

More info: www.banquedeluxembourg.com