In the past, purchasing or building a home was unquestionably a profitable decision. According to the National Institute of Statistics and Economic Studies (STATEC), Luxembourg's distribution between tenants and property owners has largely remained the same in recent years. However, the housing market has evolved significantly over the years, leading many to question whether it is in fact still profitable to buy or build your own home in the Grand Duchy these days.

Although the decision should be made on a case-by-case basis, certain criteria remain invariable. The length of stay in the country plays a role, particularly for newcomers to the Grand Duchy. In cases where foreign workers are invited to live and work in Luxembourg by their employer, they may be entitled to a rent supplement from the business. Others may only want to stay in Luxembourg for a few years before moving on. Perhaps more importantly, budget and household are key. A couple earning two salaries are less likely to have issues finding accommodation, compared to families with multiple children and pets.

Both buying and renting options therefore have advantages and disadvantages.

Although the financial burden is less when renting a house or apartment, tenants will be subjected to certain constraints and restrictions. Here are some pros and cons of renting.

Purchasing property is a big investment, which may be heavier to bear, but can offer several advantages. Here are the pros and cons of purchasing.

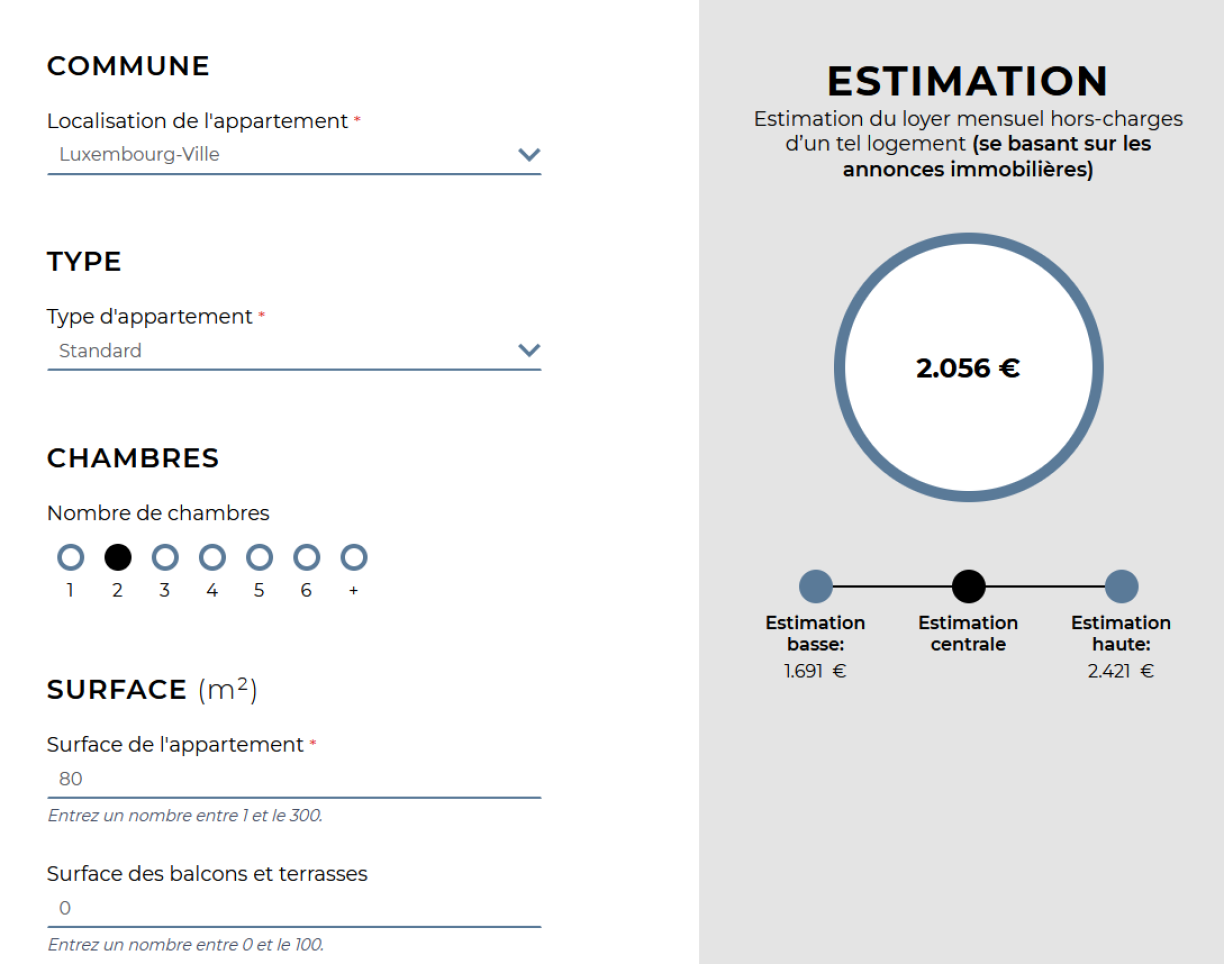

Real estate loan broker Attilio Porrini helped RTL to put together an example of rental costs, based on conditions from early August 2023.

How much would it cost to rent a two-bedroom apartment in Luxembourg City? For this purpose, we looked at how much an apartment of around 80 square metres with a parking space would cost for a childless couple in their thirties. The average price can be estimated here. According to the site, the rent for an apartment with these characteristics in the capital would cost around €2,056 euros per month, without charges.

The broker estimated monthly charges to cost around €250, with an additional €50 for insurance, which results in a monthly cost of €2,356. Over three years, this would cost €84,816, rising to over €141,000 in five years.

In order to purchase a flat in Luxembourg City, under the same conditions detailed in the example above, you would be looking at paying €780,000 to €790,000 euros, according to property website AtHome. The costs for such a property would be as follows:

| Purchase price | €789,500 |

| Deed | €5,000 |

| Registration fees | €15,265 |

| Mortgage deeds | €5,000 |

| Bank fees | €2,000 |

| Equity | €66,765 |

| Mortgage loan | €750,000 |

| Average monthly costs | €3,574 over 360 months at a rate of 4% |

The additional fees come to a total of around €27,265, to be added to the cost of the property itself. In addition, buyers must also consider life insurance, which can come to a total of around €13,580 per person if entitled to the single premium, and can be split across monthly payments or paid in one go. Paying life insurance in one go saves a tax advantage of around €3,600.

Porrini says buyers can save taxes with additional bank charges linked to the mortgage; however, this depends on how the buyer is taxed. It must also be taken into account that notary fees can vary depending on different agencies and the speed at which they work.

Mortgage interest also represents a variable cost. For the loan in the example, the buyers would pay €536,640 euros over 30 years. A variable rate would mean they would pay more in the first few years than the remainder of the mortgage.

The broker calculated the difference in costs over five years:

| Renting | Buying | Price difference | |

| Years 1 to 3 | €84,816 | €109,207 | +€24,391 €677 per month |

| Years 1 to 5 | €141,360 | €162,325 | +€20,965 €349 per month |

The obvious conclusion is that buying is particularly expensive in the first few years of the mortgage, while tenants save between €349 and €677 per month in the short term. However, this difference is exacerbated by the high interest rates at the time of writing. If interest rates fall, the situation would look somewhat different.

While a tenant may maintain their own capital, property owners must pay additional monthly costs, Porrini says. "Buying property will always be more lucrative in the long term. There are always crises or difficult situations such as the current state of the economy. Experience shows, however, that these situations stabilise over time, leading to buyers making a profit when they go on to sell their property. And even amidst the current difficult circumstances, owners can make a profit in the long term."

Luxembourg estate agent Christoph Krause agrees that property always sells, even in times of crisis. However, he says the price must be right. "The time of dreamers and exorbitant price expectations has ended."